|

||||||

| Off-Topic Lounge [WARNING: NO POLITICS] For all off-topic discussion topics. |

|

|

|

Thread Tools | Search this Thread |

07-01-2022, 01:39 AM

07-01-2022, 01:39 AM

|

#1 |

|

Senior Member

Join Date: Mar 2017

Drives: Q5 + BRZ + M796

Location: Santa Rosa, CA

Posts: 7,883

Thanks: 5,668

Thanked 5,804 Times in 3,299 Posts

Mentioned: 70 Post(s)

Tagged: 0 Thread(s)

|

The Housing Investment Paradox

Maybe this is common knowledge, and if not, I seriously doubt I am the first to talk about this subject, but there is a growing housing issue that seems to not be discussed.

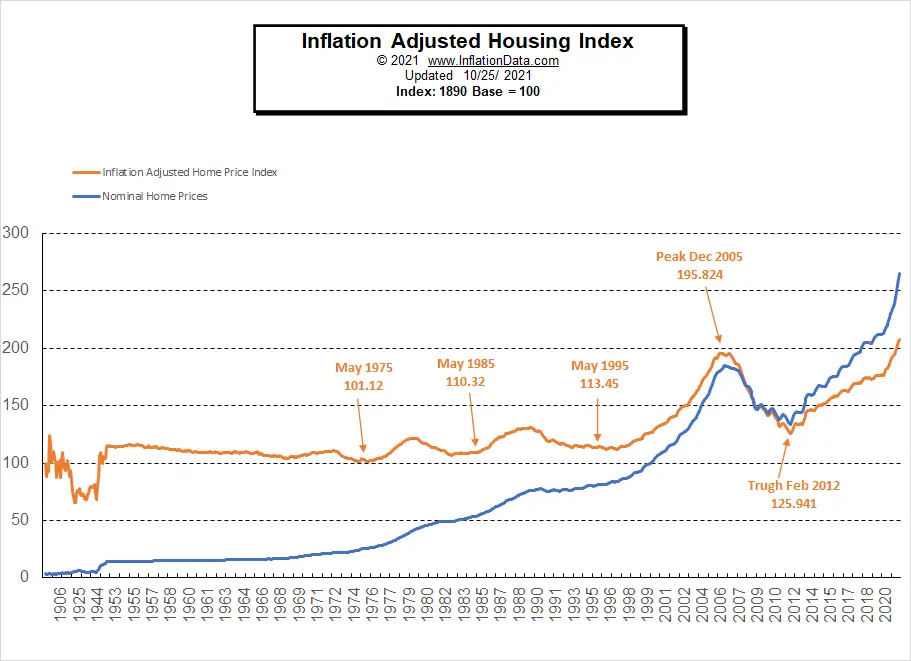

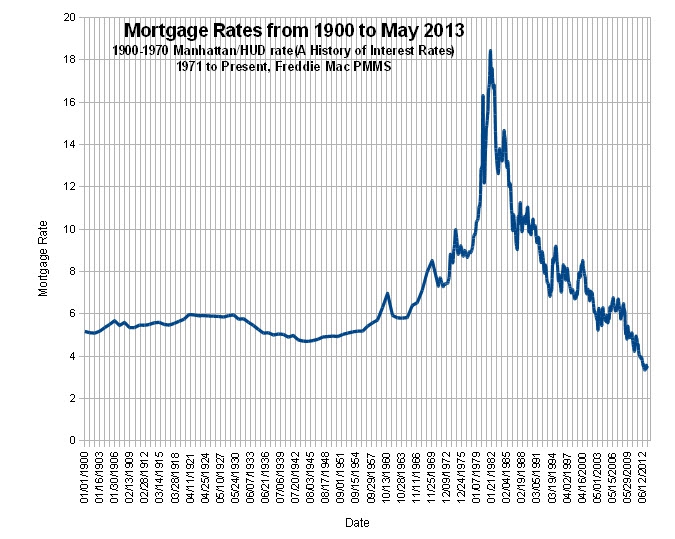

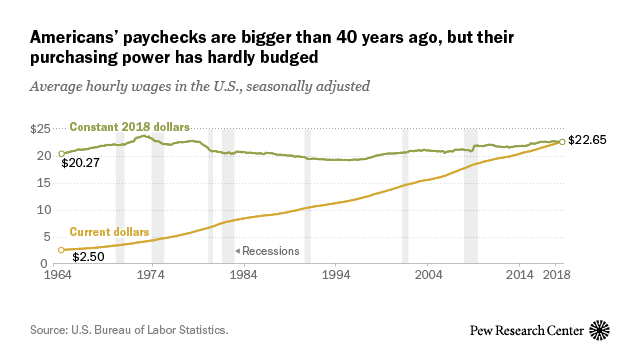

What is being discussed is that the US has a housing, supply deficit that is causing an increase in home prices and rental prices. This has been going on for some time now, far before the pandemic, extending to the Great Recession where building and investment has never really recovered. But this isn't really the problem, as I see it. What I see as the problem isn't really being discussed. Before getting into the issue, I want to explain the past because it is important to understand the problem. In the past, land/homes weren't investments; they were depreciating assets or even a liability. Why? People had little incentive to buy an old home when they could build a new home. Land and building homes were cheap, so like a car, no one wanted to pay retail value or more for an old car. Most people who buy a car today pay a certain amount, and despite improvements and maintenance, the car will depreciate. With exception to rare and valuable cars, most cars depreciate. Similarly, homes were a depreciable asset, but unlike a car, they weren't made obsolete so quickly, and the improvements and maintenance were far better to homes than cars, and for that reason, home prices stayed fairly flat. With that said, homes were still a liability more than an asset. Most people who mortgaged a home saw little to no appreciation on the home, yet they had to pay interest on their property, which means a home was a net loss over their lives, relative to inflation. They may have bought a home for $100k with 20% down and sold it for $100k, again, relative to inflation, but they may have paid 5-20% on the loan, so that could be anywhere from $80k-$400k down in interest payments. Owning a home was not a way of building wealth; it was a sign of wealth, or at least, it showed that someone could afford to buy at the expense of what was more practical--renting and investing in the stock market. It was more of a luxury. It really was part of the American dream to own. It meant someone made it. https://www.loanatik.com/827-2/ What we see below is average home prices relative to inflation were fairly flat for a long time and so was mortgage rates. Then there was little fluctuations and then things went to hell. Mortgage rates increased in response to massive inflation in the late 70's, and as you can see, we are in another round of high inflation now. This is because we had a pandemic, wages are up, demand is up, supply chains are still tight, corporations want to recoup losses from the pandemic and from wages because despite paying people more, they still need their 8-10% growth, so they are spiking prices, and in response, the fed has increased mortgage rates. How far will it go up, and what will that do to the housing market?     The other thing to note in the first graph is how we saw a housing balloon that culminated in the housing burst in 2008 resulting in the Great Recession. This was stemmed by high-risk mortgages and something else that I'll discuss in a second. For the most part, we have regulations against high-risk lending. We aren't doing crazy ARM loans or loaning to high-risk bowers. These were people that were paying a higher rate with poor credit with little down and at a high percentage of their income, and yet, here we are at the same point we were at before with home prices out of control, and this is the problem and my point: homes are being used as investments when that isn't sustainable. As I mentioned before, homes were not investments. If someone paid cash, they probably saw that investment stay flat or ever so slightly appreciate, but everyone else who took out a mortgage most likely saw their home being a depreciable asset. The only people making money on homes were people who were investing in real-estate for the means of buying to rent to build passive income, but that is really a separate issue (even if we could talk about how foreign investments in US housing is influencing the market, or how AirBnB has altered the investment market, and exacerbated a problem). Somewhere along the way, homes became an appreciable asset--an investment. While renting and investing can still prove to be better than buying, as it once was, the average rate of return on a home is near or higher than the rate of return on a standard mutual fund, so it has become one of the best ways someone can generate wealth. Outside of someone selling and buying multiple times in their life, incuring expenses and realtor fees, it is a sound investment, yet this is the paradox: if home prices are investments then they necessarily have to grow faster than the rate of inflation, yet that also necessarily means homes become less and less affordable relative to the rate of inflation of wages. If the average rate of inflation was 3.5%, for instance, and the average rate of return for a home was 8.5-10%, and say we take this to some arbitrary point in infinity, then there would become such a disparity because housing inflation outmatches wage inflation that the average home is $50 million by today's standards. The only way a home becomes affordable is if we also saw living inflation where more and more people lived in progressively smaller and smaller dwellings, such that the single room apartment that is $50 million also has 12,500 residents each paying $4k/month or 87% of their $55k average salary, before taxes. Obviously, this sounds ridiculous, but then again, when you think about it, so does the concept of homes being investments. It is a paradox. It is entirely unsustainable to have residences for the masses be investments that appreciate higher than the wages of the people that need to afford them, whether that is to buy-to-live or buy-to-rent because the investor needs to be able to recuperate their investment by renting at a profit. Something has got to give. Some people will say that wages will just increase, such that, people have more buying power today relative to tomorrow. We have cars and take trips where we once all were on horseback. Third world countries modernize and people can afford more, but this just hasn't been the case. Wages have been stagnant relative to inflation. Some goods are cheaper due to economy of scale, innovation and other factors, but buying power is relatively flat. We kind of know this because we talk about the high cost of cars on this forum all the time. Sure, a Golf GTI would destroy a Ferrari from the past, but an entry level sports cars seems to get more and more out of reach relative to the average income. This is true for buying a home. While interest rates have been higher, the idea of owning is far more impractical now than it has been at many points in the last century.  I don't know if the housing market will implode, regardless of the lack of high-risk loans. Maybe people are still over-extending themselves on what they can truly afford, or maybe investors are over-extending themselves by taking on too much liability and banking on a reliable market with stable renters. Maybe if we hadn't had foreclosure and eviction protections, we would have seen the housing bubble burst, but again, something has got to give. Whether it is an implosion, a recession, or a housing recession, or what, this is currently unsustainable. I don't know if it can persist for five years or fifty or five hundred years. I don't know if it will rise and fall in waves, but surely, this housing issue is eventually going to taper off or cause a crisis in the market or in homelessness or in civil unrest. If I am way off, please correct me. I really haven't read a whole lot of discussion on the lack of sustainability of the housing market, as an investment, but I fear this will be a real problem. Indirectly, many people don't invest and save enough in IRAs, roth IRAs, 401Ks, Bitcoin, or whatever, as it pertains to retirement. Many people sink a lot of their investments into a single asset--their home, and many rely on social security and having their home paid off to be enough, or they plan on that and some savings after selling and downsizing to a smaller home. Maybe that won't be possible. It is a paradox worth considering.

__________________

My Build | K24 Turbo Swap | *K24T BRZ SOLD*

|

|

|

| The Following User Says Thank You to Irace86.2.0 For This Useful Post: | soundman98 (07-01-2022) |

|

07-01-2022, 06:58 AM

|

#2 |

|

Senior Member

Join Date: Jan 2018

Drives: 2013 frs red

Location: South Florida

Posts: 3,517

Thanks: 2,520

Thanked 3,088 Times in 1,654 Posts

Mentioned: 6 Post(s)

Tagged: 1 Thread(s)

|

Things go up and then go down

|

|

|

|

07-01-2022, 09:44 AM

|

#3 |

|

Senior Member

Join Date: May 2014

Drives: 2017 BRZ

Location: Chicago

Posts: 3,285

Thanks: 1,256

Thanked 2,928 Times in 1,714 Posts

Mentioned: 58 Post(s)

Tagged: 0 Thread(s)

|

Far too many people like to believe some day they may be the ones to get rich quickly... And therefore support things which are not in their best interest. Borrowing from future generations is one such, and the only way housing can be an investment.

I've never considered a house to be an investment. Lots of other reasons to buy, but the math is pretty simple. It is unreasonable to expect housing to exceed inflation. Chart the wealth of the richest people and you'll see some of what's happening. But when you look at how housing as an investment works... Buying power would have to be negative over time in order for housing to be an investment. I'm starting to repeat myself so...

__________________

Second chance build... or whatever it is.

|

|

|

|

| The Following 4 Users Say Thank You to cjd For This Useful Post: |

|

07-01-2022, 09:47 AM

|

#4 |

|

The Dictater

Join Date: Apr 2017

Drives: '13 Red Scion FRS

Location: MD, USA

Posts: 9,427

Thanks: 26,109

Thanked 12,430 Times in 6,146 Posts

Mentioned: 85 Post(s)

Tagged: 0 Thread(s)

|

I think a part you are missing is that there is only so much desirable land/living space to go around. Notionally, everyone* has to live somewhere. As the population increases, there is less land per person and so the value of any land increases. So, as long as the population desiring to be in some region increases, the value of the living space will increase relative to the value of the local currency. Take a look at areas which have a depopulation problem and you will see the opposite effect.

Is it the most efficient investment, not always. But barring some great disaster it's a pretty safe bet. Values can fluctuate, but land itself will increase in value over time. Plus you can actually use land for stuff. You can't go to a Tesla factory and ask to use it for something because you own Tesla stock. But don't get me started on "depreciation" real estate tax deductions for rental properties... |

|

|

|

| The Following 3 Users Say Thank You to Spuds For This Useful Post: |

|

07-01-2022, 10:04 AM

|

#5 |

|

Senior Member

Join Date: Jul 2014

Drives: 2020 Hakone

Location: London, Ont

Posts: 69,845

Thanks: 61,656

Thanked 108,283 Times in 46,456 Posts

Mentioned: 2495 Post(s)

Tagged: 50 Thread(s)

|

I understand that you can buy homes in Gary Indiana or Detroit for $1.

As Spuds points out desirable land goes up in value everything else stays the same or goes down. My city is a great example. There are thousands of new homes being built around the outskirts and each of them is sold before they even break ground. Meanwhile the city core gets more and more empty by the year. This means it is starting to crumble and that makes it empty out even faster. You can buy property there for a song since nobody wants it. There is no shortage of inexpensive places to live just a shortage of people that will live there. The fun part is that eventually the ares get so empty and the land so cheap that developers will buy it up, build high rise luxury apartments and sell them for exuberant prices. This will then make the area desirable and people will fight to move in. The undesirable area will then move on to the next few blocks. Have seen this cycle through several times over the decade.

__________________

Racecar spelled backwards is Racecar, because Racecar.

|

|

|

|

| The Following 4 Users Say Thank You to Tcoat For This Useful Post: |

|

07-01-2022, 10:13 AM

|

#6 | |

|

Senior Member

Join Date: Jun 2020

Drives: 2018 Subaru BRZ

Location: Stonington, Connecticut

Posts: 3,281

Thanks: 1,514

Thanked 4,141 Times in 1,986 Posts

Mentioned: 24 Post(s)

Tagged: 0 Thread(s)

|

Quote:

I agree with this. I live in a very small town, very conservative in the sense of allowing food chains and major retailers, this means that is not a highly desirable area because of the lack of, say, attractions. Come December of 2019, we close on the house, sellers come down $15K, even willing to pay for closing costs. Taxes are low, $3k a year. It was a no brainer for us. Extended our work commute by like 10 minutes, longer for restaurants and shopping centers. 2020 hits, WFH is widely adopted. Now that quaint, small town is a heaven for NY, NJ, Philadelphia, and MA residents. Value of homes skyrockets. So much that last time I checked with my broker, we are $100K of increase on value of the house. I don't think I've seen a "For Sale" sign stay up for longer than 2 weeks.

__________________

God gave me an okay mind, but a really good ass, which can feel everything in a car. Nikki Lauda

|

|

|

|

|

| The Following 3 Users Say Thank You to spcmafia For This Useful Post: |

|

07-01-2022, 10:24 AM

|

#7 |

|

Senior Member

Join Date: Feb 2017

Drives: '13 Whiteout

Location: San Clemente

Posts: 1,491

Thanks: 496

Thanked 1,242 Times in 673 Posts

Mentioned: 10 Post(s)

Tagged: 0 Thread(s)

|

Lol, I built a house for a client and the cost with the land was 3m. He sold it for 12m 3 years later so houses can be lucrative. Our area is making a sh*tload of money for people.

|

|

|

|

|

07-01-2022, 11:10 AM

|

#8 |

|

Senior Member

Join Date: Jan 2020

Drives: '20 BRZ tS (15/300) / '09 Scion tC

Location: PA

Posts: 685

Thanks: 430

Thanked 826 Times in 393 Posts

Mentioned: 0 Post(s)

Tagged: 0 Thread(s)

|

I think the OP's point is about as common knowledge as a first time homebuyer understanding escrow for taxes. There are a select few in comparison to the general population that make money in real estate - just like in any business or industry. I didn't buy my house as investment... more than it was something I could control to make sure someone else wasn't profiting on my naivete.

There is something not illustrated in these charts. When mortgage interest rates were 18%, CDs were paying about 14%. All things considered equal, the spread was still 4.5%. Another thing to consider is that those coming of age in the last decade are not buying homes, cars, or expressing interest in entering politics at the rate of any generation before it. These factors are going to have a huge impact in the next 20-30 years how things play out. There won't be enough people playing the game to sustain the rate of people leaving it.

__________________

|

|

|

|

| The Following User Says Thank You to 2020BRZtS For This Useful Post: | NoHaveMSG (07-01-2022) |

|

07-01-2022, 11:52 AM

|

#9 |

|

1st86 Driver!

Join Date: Feb 2012

Drives: '13 FR-S (#3 of 1st 86)

Location: Powder Springs, GA

Posts: 19,811

Thanks: 38,817

Thanked 24,936 Times in 11,375 Posts

Mentioned: 182 Post(s)

Tagged: 4 Thread(s)

|

@Irace86.2.0 I believe your theory about new vs existing home sales is incorrect, at least in the US. The existing home sales far exceed new home sales.

New home sales in May were 696,000 units. Existing home sales was 5,410,000 according to the source I linked above.

__________________

Visit my Owner's Journal where I wax philosophic on all things FR-S Post your 86 or see others in front of a(n) (in)famous landmark. What fits in your 86? Show us the "Junk In Your Trunk". |

|

|

|

| The Following 4 Users Say Thank You to Dadhawk For This Useful Post: |

|

07-01-2022, 01:07 PM

|

#10 |

|

Senior Member

Join Date: Mar 2017

Drives: Q5 + BRZ + M796

Location: Santa Rosa, CA

Posts: 7,883

Thanks: 5,668

Thanked 5,804 Times in 3,299 Posts

Mentioned: 70 Post(s)

Tagged: 0 Thread(s)

|

Again, it really doesnt matter how desirable something is if no one can afford it. We might all like to own Ferraris and Porsches, but we all dont because we lack the money.

The fact is housing inflation/investment cant grow faster than the rate of inflation/growth of wages forever or the average home would be $50 million relative to todays money, eventually. Regardless of desirability, the average home just wouldnt be affordable. There could be pockets of affordable housing and pockets of unaffordable housing, but the average home would necessarily be unattainable, or it will be not an investment; it will be something that only grows at the rate of inflation of wages, which is to say, it will be flat relative to inflation. Im sure someone could actually calculate when the cost would be prohibitive for the average person to qualify for a 0% interest mortgage with a DTI of 50%. If the median household income is $106k per year, the median home price is $375k and housing inflation outpaces wage inflation by 4%, at what point would the median household be unable to qualify for a mortgage, or rather, in how many years would the DTI be greater than 50% on a mortgage? Who wants to do the math?

__________________

My Build | K24 Turbo Swap | *K24T BRZ SOLD*

|

|

|

|

|

07-01-2022, 01:21 PM

|

#11 |

|

The Dictater

Join Date: Apr 2017

Drives: '13 Red Scion FRS

Location: MD, USA

Posts: 9,427

Thanks: 26,109

Thanked 12,430 Times in 6,146 Posts

Mentioned: 85 Post(s)

Tagged: 0 Thread(s)

|

A location that is too expensive for a working class to support it very quickly becomes undesirable. Everyone who is left in that area loses out big in the resulting crash. Like a forest fire, that clears the way for new growth and the cycle repeats.

One reason why a lot of people are leaving California. Moral of the story, don't be there when the meteor hits. |

|

|

|

| The Following 2 Users Say Thank You to Spuds For This Useful Post: | soundman98 (07-01-2022), Wally86 (07-06-2022) |

|

07-01-2022, 01:25 PM

|

#12 | |

|

Senior Member

Join Date: Mar 2017

Drives: Q5 + BRZ + M796

Location: Santa Rosa, CA

Posts: 7,883

Thanks: 5,668

Thanked 5,804 Times in 3,299 Posts

Mentioned: 70 Post(s)

Tagged: 0 Thread(s)

|

Quote:

__________________

My Build | K24 Turbo Swap | *K24T BRZ SOLD*

|

|

|

|

|

|

07-01-2022, 01:28 PM

|

#13 | |

|

Senior Member

Join Date: Mar 2017

Drives: Q5 + BRZ + M796

Location: Santa Rosa, CA

Posts: 7,883

Thanks: 5,668

Thanked 5,804 Times in 3,299 Posts

Mentioned: 70 Post(s)

Tagged: 0 Thread(s)

|

Quote:

__________________

My Build | K24 Turbo Swap | *K24T BRZ SOLD*

|

|

|

|

|

| The Following User Says Thank You to Irace86.2.0 For This Useful Post: | Spuds (07-01-2022) |

|

07-01-2022, 01:36 PM

|

#14 |

|

Senior Member

Join Date: Aug 2014

Drives: '23 BRZ Limited

Location: OKC, OK

Posts: 1,986

Thanks: 660

Thanked 1,229 Times in 702 Posts

Mentioned: 9 Post(s)

Tagged: 1 Thread(s)

|

One thing your failing to bring up when owning vs renting and I do believe a home is a liability, because anything that costs you money is a liability.

I bought my home here in OKC almost 5 years ago. The payment is the same then as it was when I made the first payment. The fancy downtown apartment I rented when I first moved here at the beginning of 2017 is roughly $300/more per month than January 2017. And most properties like that go up each time you renew your lease. But I also don't have to replace the AC unit if it goes out, or pay the deductible if a hail storm trashes my roof. And as far as I gather, many people will buy a home vastly too expensive for their income just because the bank will loan it to them. That's one of the few things that keeps me in Oklahoma. I purchased a nice, completely renovated home in a quiet neighborhood, for $156k. So my month payment is only about 22% of my take home, vs the 30-35% gross banks will lend you. And that doesn't include my fiance's salary.

__________________

"95% of the time, more throttle is the answer. 5% of the time, it ends the suspense."

|

|

|

|

| The Following User Says Thank You to OkieSnuffBox For This Useful Post: | Wally86 (07-06-2022) |

|

|

|

Similar Threads

Similar Threads

|

||||

| Thread | Thread Starter | Forum | Replies | Last Post |

| PTE 6466, 1.0 divided A/R, polished comp housing, black ceramic turbine housing | slicktop | Engine, Exhaust, Bolt-Ons | 6 | 10-17-2015 10:53 PM |

| 63-67 corvette as an investment | mike the snake | Other Vehicles & General Automotive Discussions | 58 | 11-13-2014 01:17 PM |

| porsche 918 spyder investment? | Rocket.BRZ | Off-Topic Lounge [WARNING: NO POLITICS] | 60 | 08-06-2014 09:18 PM |

| Are components worth the investment? | Cmeehleib5280 | Electronics | Audio | NAV | Infotainment | 25 | 03-31-2014 01:27 AM |

2020 Subaru BRZ tS

2020 Subaru BRZ tS